The conventional way Treasury and independent economists look at ICT industry employment and contribution to GDP – often, confusingly referred to as ‘the tech sector’, or ‘the digital economy’, or almost any other euphemism to avoid saying ICT – is to look at the industry division statistically called IMT (Information, Media and Telecommunications).

They do this because ICT, for historical reasons, does not have an official industry division in its own right, despite being one of the larger employing industries in Australia.

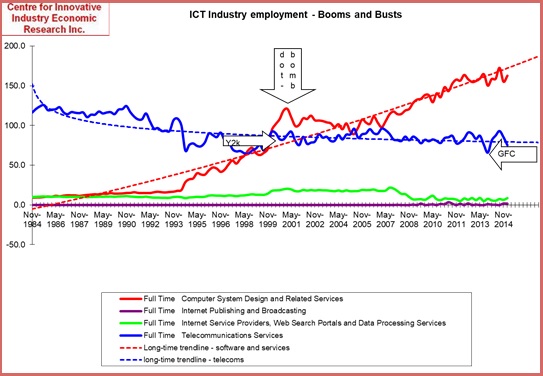

The ANZSIC IMT division, however, only includes telcos and ISPs, but excludes the far larger employment in the software and services sector of the ICT industry, (as well as the tiny ICT retail and manufacturing sectors), as even the most cursory look at the Australian Bureau of Statistics Labour market data easily reveals.

The chart below, derived from that data shows that, since around 2003 – coincidentally the last time the Australian Bureau of Statistics calculated the ICT industry contribution to Australian GDP at 4.6% – the telecommunication sector continued to decline, at the same time as software and services employment continued to grow, such that by 2014, Software and Services employment was twice that of Telecommunications, in an ICT industry employing well over 350,000 Australians.

Those long term trendlines have continued, regardless of economic ‘blips’, to a variance in 2019 of two-and-a-half, with ACS Deloitte Digital Pulse reporting 101,649 people employed in telecommunications companies, and 248,915 employed in software and services companies.

A perverse outcome of this blindness is that the official data provided by our Government to international bodies like the OECD on ICT performance in Australia leads such agencies to incorrectly compare Australia IMT Division performance to the actual ICT performance of other nations.

This leads otherwise reputable economic analysts in Australia to look at our OECD reported performance and to draw incorrect conclusions.

It was claimed in one much cited report in 2019, that ICT made a contribution of only 2.8% to Australian Gross Value Added (GVA), and that this was only just better than Mexico.

And compared to a country like France or UK – currently at around 7.5 to 8% of GVA – we were failing badly. Note that ABS calculated our performance in 2003 at 4.9%, from a then much smaller industry.

Of course, this is nonsense and any accurate calculation of Australia’s ICT industry GVA or GDP contribution would almost certainly have us ranked far higher, probably higher than UK for example, as our employment ratio is a little above theirs.

But until the ABS is allowed to do the calculation, we will probably never know.

One could ask why our Australian ICT industry should be castigated for poor performance, when the fault is that our mandarins in Treasury simply don’t understand the numbers they are looking at – and likely advise the Government accordingly – and our leading statistics agency has failed to provide up-to-date information.