Despite its size and resources, the National Australia Bank (NAB) still can’t provide accurate data to users of Consumer Data Right (CDR) services – leading it to cop a record $751,200 fine amidst industry concerns that Australia is missing out on the benefits of open banking.

The ACCC fine – the largest such fine ever meted out for violations of the CDR infrastructure that supports Australia’s ‘open banking’ regime – stems from four cases where the NAB failed to provide accurate information about CDR consumers’ credit card limits.

This, in turn, affected the ability of numerous CDR data recipients to use that data for mortgage broking and other fintech services, compromising the efficacy of a five-year-old data sharing regime that was designed to empower consumers to switch financial products.

CDR rules provided for a fixed penalty of $187,800 at the time of the errors (since increased to $198,000), putting the bank on the hook for nearly $1 million in fines for just four instances of inaccurate data.

The NAB penalty is the second recent case to highlight just how seriously the government takes data accuracy, with ACCC earlier this month blaming Regional Australia Bank (RAB) for a third-party data mix-up that it did not cause and knew nothing about.

“Poor data quality prevents consumers from experiencing the full benefits of the CDR,” ACCC deputy chair Catriona Lowe said in announcing the penalty.

“When banks or energy retailers don’t provide accurate data, consumers can’t take advantage of CDR products and services.”

Formal CDR data standards were launched several years ago and “data holders have had several years to understand and implement their CDR obligations,” she said, noting that “all CDR participants are reminded that failure to comply...will result in scrutiny by the ACCC.”

Inertia compromising the benefits of digital finance

The Australian government has a lot riding on the success of CDR, which is a showpiece of its digital services innovation but has undergone multiple tweaks after struggling to gain consumer traction.

There are signs those efforts may be working: more than 530,000 consumers successfully used CDR in the banking and energy sectors during the second half of 2024, ACCC said – up 135 per cent over the previous half year – and 582 million CDR requests were made.

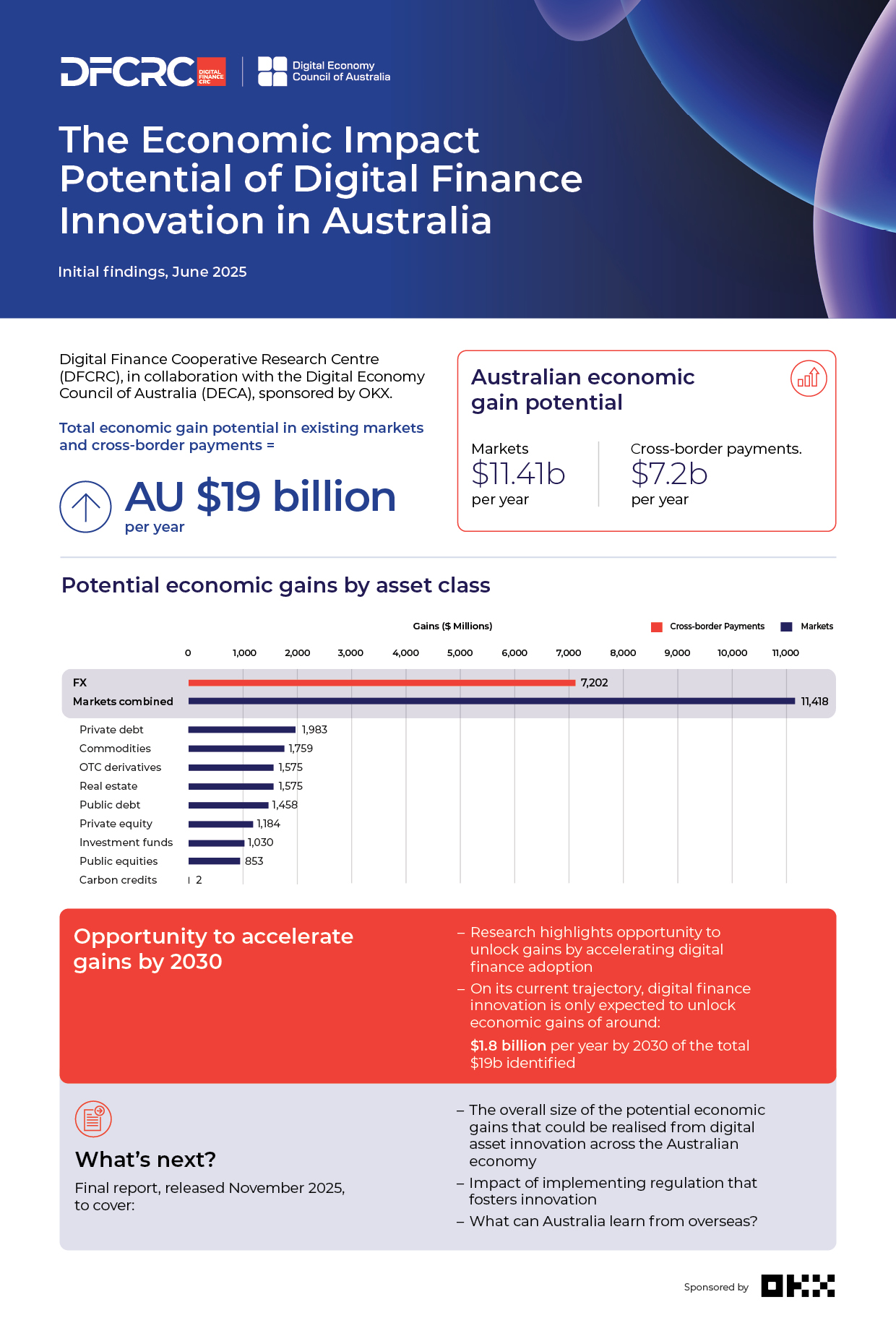

A lack of momentum around open banking is exerting significant drag on Australia’s digital finance innovation, according to a new report from the Digital Finance CRC (DFCRC) that found Australia’s finance market is likely to realise only 10 per cent of its potential by 2030.

Markets’ accelerated adoption of digital finance options could generate $11.4 billion in economic value – and $7.2 billion more from cross-border payments – but “on its current trajectory,” DFCRC only expects digital finance innovation to unlock $1.8 billion in new value.

“Adoption of digital finance innovation requires substantial industry-wide change that take time,” it noted, adding that additional value “could be achieved through innovation-enabling regulatory and policy initiatives and greater industry-wide collaboration.”

Australia “isn’t currently on track [and] is at a pivotal juncture for digital finance globally and has a strategic opportunity to capitalise on this and position itself as a competitive, innovation-friendly financial hub,” DFCRC chief scientist Tālis Putniņš said.

Getting serious about CDR at last?

Like payment innovations such as instant transfers, CDR has been a key part of this transformation – yet open banking’s struggles here, which echo similar issues in the UK , show just how much inertia is affecting the government’s digital payments agenda.

Aiming to jumpstart use of open banking, Westpac New Zealand this month announced that it would promote the rollout of open banking in that country by providing accredited third-party providers with free access to its data-exchanging APIs.

Allowing fintechs to integrate into our open banking APIs for no cost should create a more affordable business model for them,” Westpac NZ CIO Russell Jones said, and “speed up access for Kiwi customers to a wide range of affordable open banking experiences.”

After past “laughable” fines such as the $53,280 penalty issued to ING in 2022, Jill Berry, CEO of CDR participant Adatree said the amount of the NAB fine is an encouraging sign that ACCC is getting serious about ensuring CDR is implemented and run accurately.

“Before when they’ve come out with fines, they’ve been absolutely laughable, but this was actually a large fine,” Berry told Information Age, suggesting that the NAB failing may have been “more about the unknown unknowns than blatant disregard for the rules.”

“Regulators are actually being really proactive right now,” she said, referencing ACCC’s RAB finding and adding that “it is good in principle that the regulators are actually regulating because the only way that people will use CDR is if they can rely on it.”

{kind=link}